.png)

Navigating the Natural Capital Revolution: A Strategic Market Analysis and Roadmap for Nature Data and Analytics

As we enter 2026, the market for nature-related data and analytics has reached a turning point. What was once a peripheral concern for corporate social responsibility departments has now become a central issue for chief risk officers, chief financial officers, and institutional investors. This shift is not speculative; it is driven by the undeniable quantification of nature's role in economic stability and the subsequent response from regulators and capital markets.

While often categorised within the broader "Climate Tech" or "Green Technology" markets, Nature Tech represents a distinct and rapidly emerging investment and product category. Climate change, despite its complexity, centres on a single, globally fungible metric: a tonne of carbon dioxide equivalent (CO₂e). This allows for standardised accounting and relatively straightforward risk modelling.

Nature, in contrast, is fundamentally different. It is hyperlocal, multifaceted, and non-fungible. The value of an ecosystem service, like water purification, is specific to its watershed.

The biodiversity risk associated with a mining operation in the Amazon is entirely different from that of a data centre in a water-stressed region of Texas. This inherent complexity creates a significantly higher barrier to entry for data providers and necessitates specialised solutions.

The Nature Tech ecosystem encompasses a range of solutions, including biodiversity monitoring, water risk management, deforestation tracking, and regenerative agriculture technologies. The data and analytics platforms that provide the intelligence required to manage risk, report on impacts, and direct capital effectively sit at the heart of this ecosystem.

Three interconnected forces came to a head in 2025, collectively pushing nature-related risk past the threshold of financial materiality.

First, the economic materiality of nature loss is now quantified and undeniable. Over half of the world's Gross Domestic Product (GDP), an estimated $44 trillion, is moderately or highly dependent on nature and its services. The degradation of these services is no longer a distant threat but an immediate economic risk. The World Economic Forum's 2023 Global Risks Report ranks biodiversity loss as the fourth most severe global risk over the next decade.

In the United Kingdom, a first-of-its-kind analysis projected that continued nature degradation could lead to a 12% reduction in GDP, a larger economic shock than the 2008 global financial crisis or the COVID-19 pandemic. Similarly, the European Central Bank found that 75% of bank loans in the Euro area were extended to companies with a high dependency on at least one ecosystem service. Through 2025, these projections began translating into practice, with several major financial institutions stress-testing their portfolios against nature-related scenarios for the first time.

This quantification has irrevocably shifted the conversation from environmentalism to core macroeconomic and financial stability, compelling action from the highest levels of government and finance.

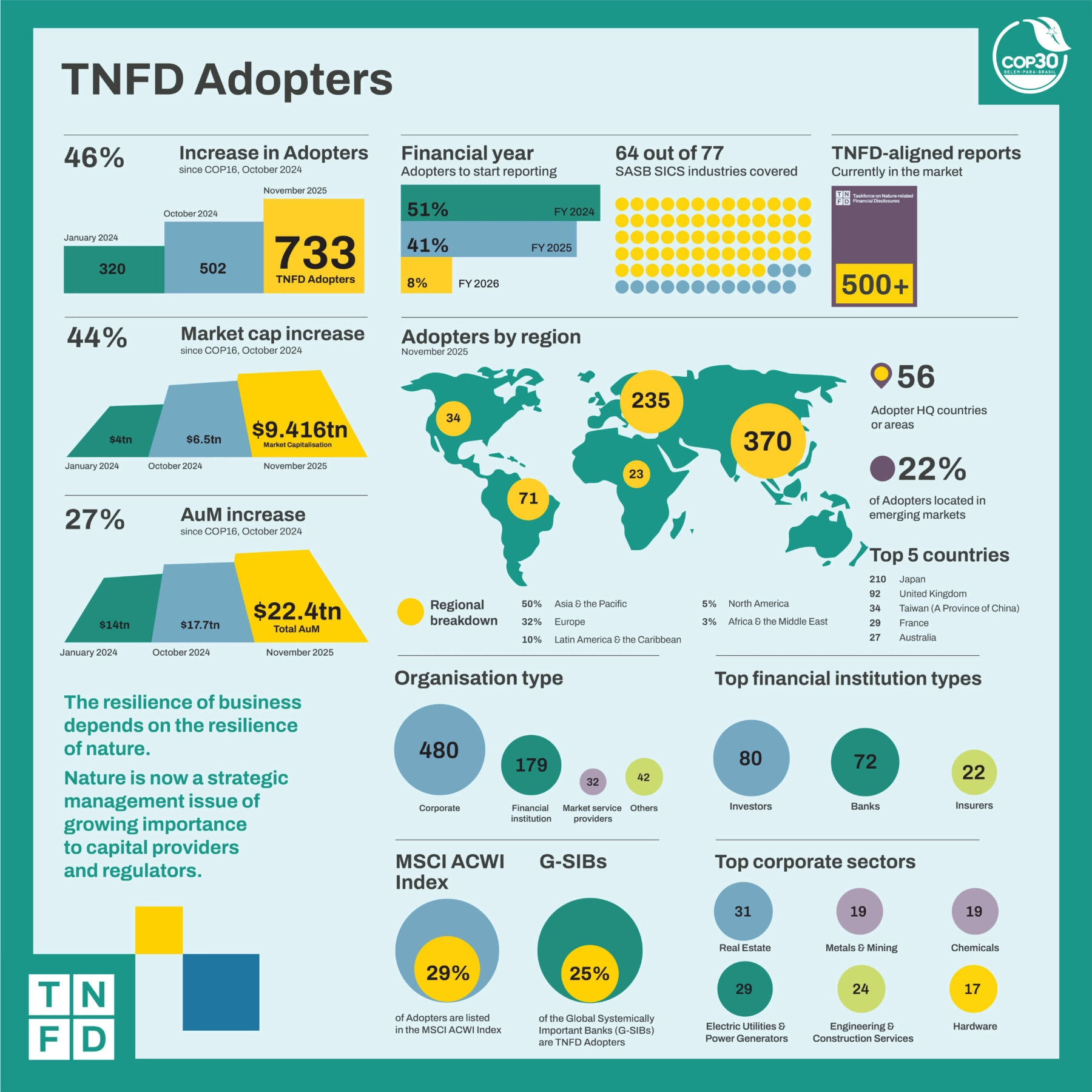

Second, regulatory mandates are transforming voluntary initiatives into legal obligations. The Taskforce on Nature-related Financial Disclosures (TNFD), launched with G7 and G20 support, has established a global baseline framework for reporting. This framework is now being codified into binding law in key jurisdictions. The European Union's Corporate Sustainability Reporting Directive (CSRD) is the most prominent example, creating a massive, compliance-driven market for nature data. Phase 2 reporting requirements took effect last year for thousands of additional companies, moving the compliance question from abstract to immediate. The momentum is global, with over 700 major organisations (including asset managers overseeing $22.4 trillion in assets under management and publicly-listed companies with a total market capitalisation of $9.416 trillion.) committing to adopt TNFD-aligned reporting.

Third, investor and financial institution pressure is creating powerful market-based demand. Supranational bodies like the Network for Greening the Financial System (NGFS), a coalition of central banks and supervisors, now officially recognise nature degradation as a source of systemic financial risk, compelling the institutions they regulate to build capacity in this area. In response, financial institutions are forming powerful coalitions, such as the Finance for Biodiversity Pledge and Nature Action 100, committing trillions in AUM to assess and manage these risks within their portfolios. The result is direct demand for analytical capabilities to screen investments, engage with portfolio companies, and report to stakeholders, a trend that accelerated sharply in the final quarter of 2025.

Supply chains have become the most pressing challenge. Without proper traceability, companies have little real visibility into their nature-related exposures. Pressure is mounting for transparency that extends beyond direct holdings to second- and third-tier suppliers, what some are calling "nature KYC." This could turn current blind spots into sources of competitive advantage.

The companies moving fastest on supply chain nature-risk mapping are pulling ahead, whilst those lagging face growing scrutiny from regulators and investors who understand that most nature-related impacts occur deep in supply networks, well beyond the direct operations that traditionally receive attention.

The entire global effort to halt and reverse nature loss, and to align financial flows with nature-positive outcomes, is fundamentally dependent on the quality and availability of data. Credible Monitoring, Reporting, and Verification (MRV) is the essential infrastructure upon which this new economy is being built. Without robust, trusted, and scalable data, capital cannot be allocated efficiently, risks cannot be managed effectively, and compliance with emerging regulations cannot be demonstrated.

The technological enablers for this data revolution are now mature. The convergence of Artificial Intelligence (AI), cloud computing, advanced geospatial analytics powered by satellite imagery, and novel techniques like environmental DNA (eDNA) allows for the scalable, accurate, and near-real-time data collection that the market requires.

Crucially, the market is rapidly moving beyond high-level, qualitative assessments and sector-level proxies. Financial institutions now recognise the need for granular, asset-level analysis. They must understand the specific water risk of an individual semiconductor factory, the deforestation footprint of a particular agricultural supply chain, or the biodiversity impact of a single mining operation within their portfolios. Providing this level of decision-useful, location-specific intelligence is the core value proposition that the market now demands.

Consequently, the dialogue with customers is shifting from a narrative of "doing good" to one of "managing material financial risk." Nature data platforms are no longer ESG add-ons. They are becoming essential risk management tools, comparable to credit rating services or market data terminals.

The path forward is not without obstacles. Questions persist about data standardisation, methodology transparency, and greenwashing prevention. The coming twelve months will test whether the infrastructure being built can deliver the reliability and comparability that capital markets demand. Success depends on more than technology: it requires sustained collaboration between data providers, standard-setters, and end users.

The transition to a nature-positive global economy represents one of the most significant economic and financial transformations of the 21st century. Nature data and analytics is not merely a component of this transition; it is the critical infrastructure upon which the entire system will be built. It is the enabling technology that will allow for the redirection of trillions of dollars of capital toward the protection and restoration of natural ecosystems.

In 2026, those who have invested in robust nature data infrastructure (both financial institutions and technology providers) will be better positioned not just for compliance, but for the nature-positive economy now taking shape. The market is ready, the regulatory framework is in place, and the window to establish leadership remains open. For those prepared to act with speed, methodological rigour, and commitment to data quality, the opportunity is clear.

.jpg)

.jpg)